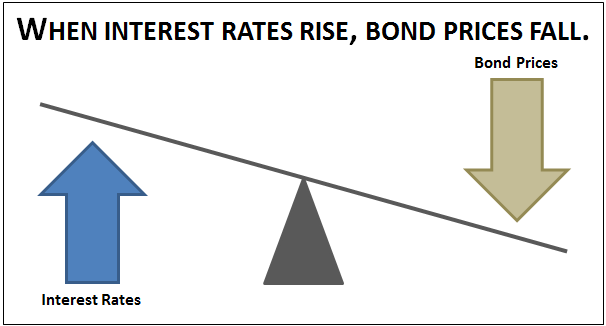

Bond See-Saw

If you took economics, you might remember a concept called “The Bond See-Saw.” For those who have no idea of what I’m talking about, let me offer a simple explanation. Picture a see-saw (or teeter totter, if you’re from the Midwest) with bond prices on one end and bond yields (interest rates) on the other. If the price of the bond goes up, the yield goes down, and vice versa. So, when you hear that the Federal Reserve is raising rates, you know that bonds, that are currently issued and owned by someone, will go down in value.

Silicon Valley Bank

If you keep up with current economic events, then you know that the Silicon Valley Bank based in San Francisco collapsed last week and was shut down over the weekend by the FDIC. Signature Bank of New York was also taken over by state regulators over the weekend.

SVB had taken part of their customers’ deposits and invested them in long-term government bonds that were paying close to 0% interest. While that doesn’t seem like a good idea to me, maybe they had their reasons . . . As interest rates have risen over the last year, the value of those bonds continued to decrease (thus the see-saw effect) to the point that last week the bank reported over a $1.8 billion loss. As a result, their stock began to sell off, and it lost $160 billion in value in just 24 hours. All this resulted in a “run on the bank,” meaning the depositors withdrew money as fast as possible, but the bank did not have the cash available to meet all of those requests.

When banks get in this kind of trouble, the FDIC steps in and takes over the bank, which is exactly what happened. The banks did not survive, but the FDIC did guarantee all the depositors’ money.

KPMG Audit Questions

Oddly enough, KPMG, a large accounting firm, had recently audited both of the banks. SVB’s audit was signed of on two weeks before their collapse and Signature Bank a mere 11 days before their issues came to light. It seems like either bank’s potential issues would have been discovered in the audit and a warning would have been issued, but that wasn’t the case.

Questions Raised

Much more information will be coming out in the weeks and months ahead about the many tentacles of this situation, but, currently, here are the questions that come to mind:

- Both of these banks did a lot of business with Venture Capitalists groups, startup companies, and the world of crypto which, because of the riskier nature of those businesses, contributed to their problems. The question now is, how many other banks are in the same situation?

- Will the Federal Reserve will continue its current policy of raising interest rates as aggressively, or will it take a step back due to the negative fallout these policies have helped create?

- Lastly, what kind of opportunities has this created for investors, and how can we take advantage?

*************

This post is for informational purposes only. It is not intended as investment advice as each person’s financial situation is different. I strongly recommend working with a financial advisor who can deliver current information to you quickly and offer help with sorting through the various investing options. Bret Wilson is a Financial Advisor with Wilson Investment Services, based in Rockwall, Texas.