Current Conditions

All eyes are still on the Federal Reserve right now. The expectation for the November meeting this week is that the Federal Reserve will raise interest rates 75 basis points. A month ago, the Fed clearly sent the message that they would do whatever they had to do to get inflation under control; they warned consumers to expect a 75-to-100 basis point rise in rates in November and at least another 50 basis points in December.

Fed Pivot?

A couple of weeks ago, the Fed initiated a leak to The Wall Street Journal that rates would be raised on the low end at 75 basis points with another 50 in December. The leak gave the impression that the Fed might be slowing down their rate increases going into 2023 and this information fueled a rally in the markets. If this week’s post Fed meeting statement does not confirm a Fed “pivot” from their hawkish stance in October, the markets are likely to begin falling again.

Need More Evidence

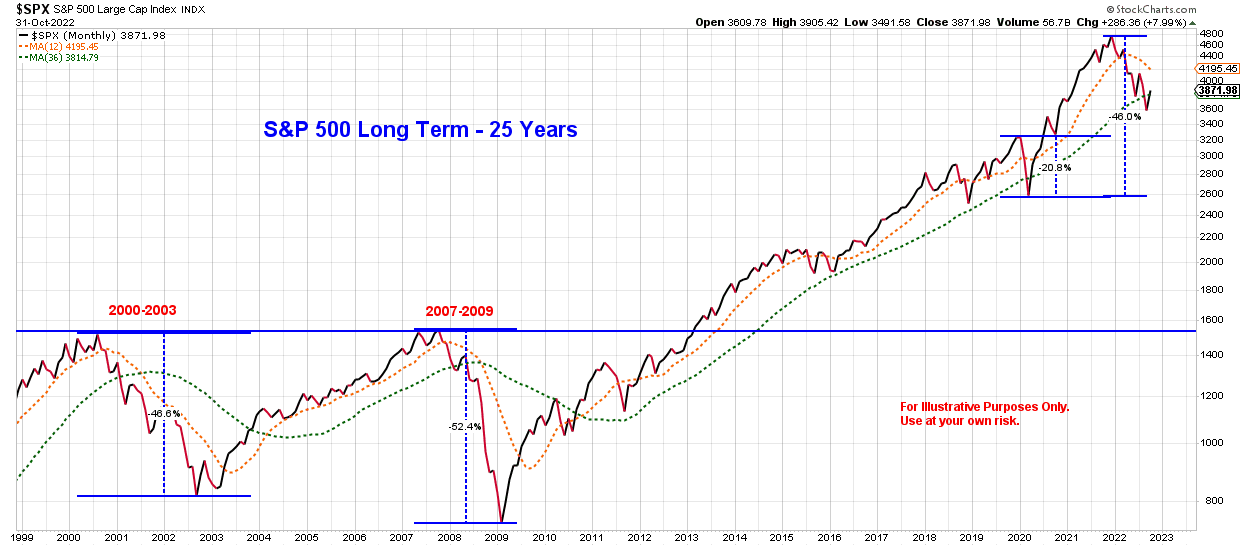

At the beginning of October, I presented the chart below and mentioned that I was concerned because “the last time the 12-month moving average line turned down like this was at the beginning of the 2000 dot-com bubble and the 2008 financial crisis.” Here we are, one month later, and not a lot has changed except the price of the S&P has climbed back over the green dotted line (36 month moving average) based on market speculation of future Fed actions. I certainly love to see a rally in the markets, but there still isn’t enough evidence to suggest that this rally will hold.

What is the Fed Up To?

You may remember the term “Quantitative Easing” (or QE) from 10 to 12 years ago during the Great Recession. This monetary policy would involve the Fed buying securities from its member banks; this action would add liquidity or cash to the banks, which could be lent out. Along with lowering interest rates, this would stimulate the economy.

Currently the Fed is engaged in the opposite of QE, which is “Quantitative Tightening” (or QT). It is selling its assets, thus removing and reducing cash from the banking system and the economy. Adding this to rising interest rates and the economy will slow down as the cost to borrowing money has now risen. This will also cause stock markets to fall which is what we have all been experiencing in 2022.

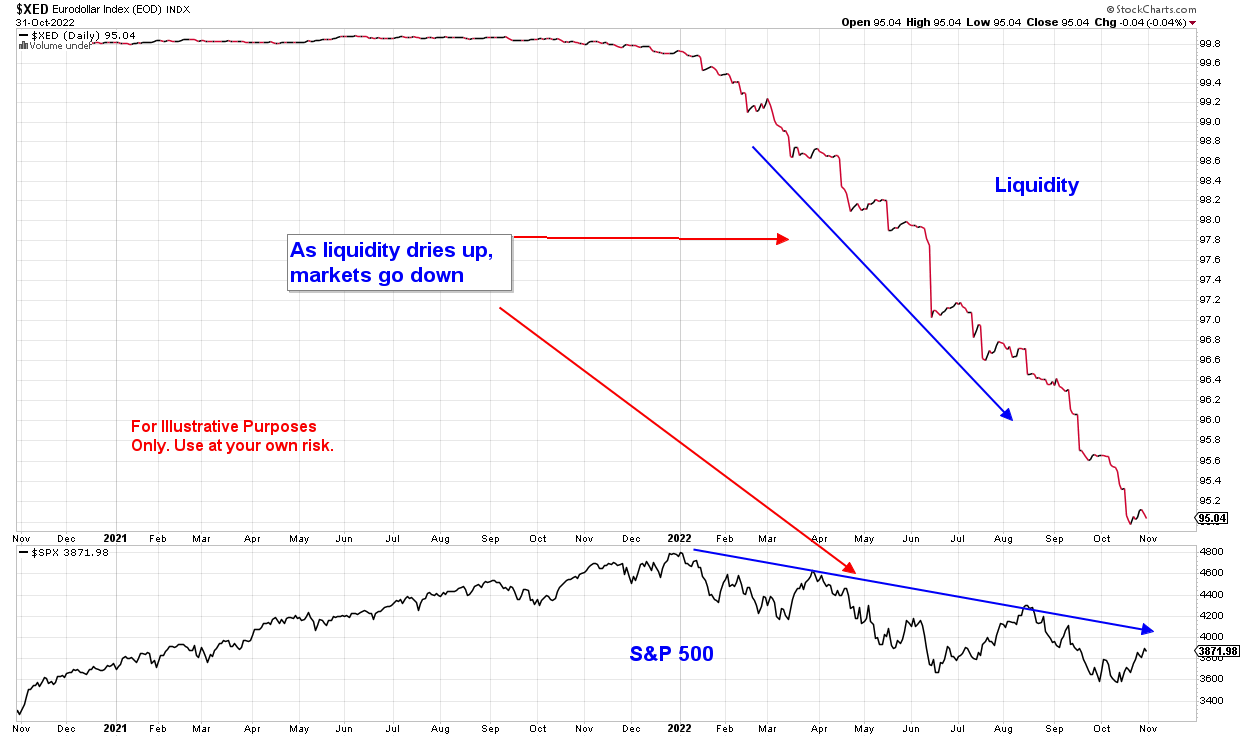

Simply put, if the chart, the Eurodollar Index, is trending down, then liquidity is drying up as the Fed intended. This means there are fewer dollars available to borrow and invest which results in a falling stock market.

I think we are currently experiencing a bear market rally that will eventually run out of steam, and markets will test their lows again. Until evidence presents itself to indicate otherwise, I will remain cautious, but as always flexible.

Disclaimer

This post is for informational purposes only. It is not intended as investment advice as each person’s financial situation is different. I strongly recommend working with a financial advisor who can deliver current information to you quickly and offer help with sorting through the various investing options.